It is currently one of the best periods ever to start an eCommerce business. The industry is booming as online sales see regular growth every year. During the Covid 19 pandemic, this trend was supercharged and consumers’ demand for online shopping hasn’t abated since.

One of the biggest hurdles that small eCommerce sellers face is having big, ambitious ideas, but not the capital to make them happen. It is hard to establish yourself in the business when your online store is still in its infancy. You can’t invest in things that will improve your business when you don’t have the income to finance it yet. Some companies have great products that fly off the shelves, while still lacking the money to send in enough orders ahead of time. So they end up running out of stock, right when their products are selling the most. It is for these reasons and more that many online sellers take out a loan in order to uphold their business growth. In this guide, we will explain the ins and outs of eCommerce loans and whether taking one out is the right eCommerce funding solution for you.

In this article we will go over:

- What are eCommerce loans?

- Why do companies take out eCommerce loans?

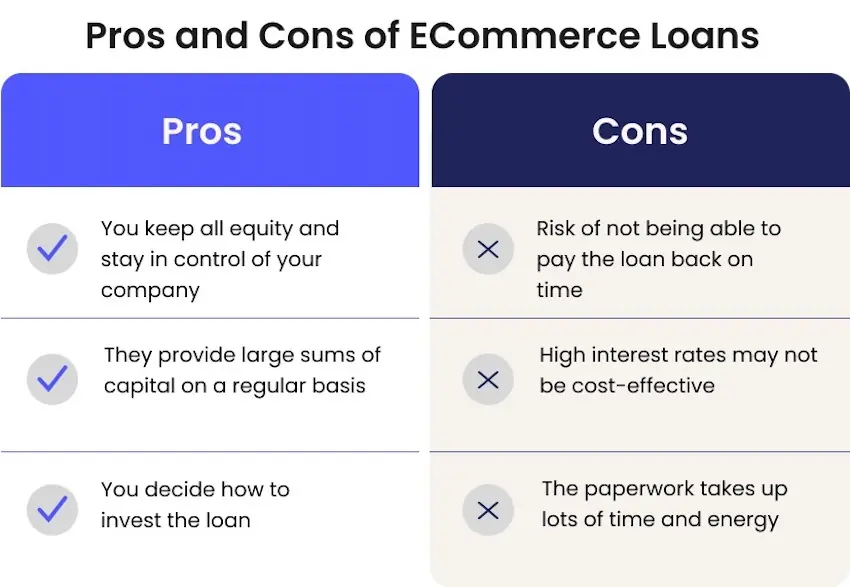

- What are the benefits of eCommerce loans?

- What are the potential downsides of eCommerce loans?

- How does a business qualify for an eCommerce loan?

- What kinds of eCommerce loans are there?

- What is the best option for you?

- A different solution

What Are ECommerce Loans?

When people talk about eCommerce loans they mean a cash sum that is lent to online retail businesses by financial institutions like banks and repaid over a mutually agreed time period. Like with most types of loans, they come with interest and certain conditions. This is unlike equity financing, where you sell business shares to investors for cash that you can reinvest. Taking a traditional eCommerce loan means that you keep 100% of your company.

However, if you are unable to repay the loan in time, the lender can take over parts of the business that were given as collateral, such as company equipment. To qualify, you might also need to give a personal guarantee, which means you personally will be liable to repay the loan if your business is unable to. The conditions of the loan will depend on your credit score and company performance. The better you are at showing that you have the financial capability to pay back your loan on time, the better the conditions will be, as it lowers the risk the lender is taking by giving you money.

Why Do Companies Take Out ECommerce Loans?

Taking such a loan can allow a business to invest in things like bigger or more frequent freight shipments, improved marketing or new products. Such steps can put the company on a long-term growth path that is worth whatever interest has to be paid on the loan.

One of the most frequent headaches for growing online sellers is managing their cash flow. Especially when products are selling fast it can be hard to keep up with inventory shipments, which often come from overseas, take a lot of time to arrive, and are prone to disruptions and delays. No one wants potential and eager buyers to face an ‘out of stock’ message and then proceed to buy from a competitor.

What makes such a situation even more frustrating is that marketplaces like Amazon are guaranteed to rank your store lower on its search results, while raising that of the competitor’s store that made the sale. Positive momentum from months of great sales and successful ad campaigns that helped you climb the search ranks can be wiped out by a poorly-timed stockout. Amazon wants its customers to see products they can buy right away, and constantly adjusts its search results according to who is out of stock and who isn’t.

The eCommerce world is fast-paced and highly competitive, so making sure your business is growing and reinvesting profits into new ways to perform better is crucial. An online seller that relies on profits from one batch of merchandise to purchase the next simply doesn’t have the ability to make the multiple advance payments that guarantee new shipments are consistently on the way. This is where a loan, combined with a reliable business strategy can work wonders.

Investing in things like better products, faster shipping, improved packaging, analytics services or stronger marketing can take an eCommerce seller to the next level. Taking such steps forward at the right time can mean a significant increase in revenue while ironing out issues in the supply chain. That momentum then carries over to Amazon where your store can reach a great keyword ranking while building a community of customers that offer helpful reviews and are happy to buy from you again, creating continuous positive growth.

What Are the Benefits of ECommerce Loans?

ECommerce loans can give online sellers access to funds they might otherwise not have. Being able to invest in the right technologies, products or processes can generate thousands of dollars down the line. This is a particularly good strategy nowadays since the eCommerce industry is growing immensely without any signs of slowing down. In fact, it is set to increase by 10.4% in 2023 according to an eMarketer study. Online purchases now make up 20.8% of all retail sales, another figure that is only set to grow going forward. Entering this thriving market and establishing yourself now can lead to significant success further down the line. There are huge opportunities for sellers with a good business strategy and enough capital to make their ideas come to life.

Having this kind of cash on hand can allow you to make serious investments in your business and how it operates. Many sellers use loan capital to shore up their supply chains by ordering more frequent freight shipments, upgrading their transport procedures to reduce product shipping times, or opening new product lines. Another surefire way to maximize the impact of new capital is to invest in marketing technology and larger ad campaigns to bring in more customers.

What Are the Potential Downsides of ECommerce Loans?

While the possibilities created by taking an eCommerce loan are numerous, it is important to remember that there are several potential drawbacks to keep in mind. You should have developed a good business plan and a solid understanding of the market you are going into before investing large sums. Ideally, your products would be selling well already, with a sturdy supply chain behind it.

The goal is to build a reliable stream of income that is solid enough to withstand disruptions and shifting trends in the market. If you sell surfboards that are flying off the shelves in summer, don’t expect those numbers to continue into winter. One of the best places to spend new funds is a line of products that are already selling well and likely to continue doing so. Alternatively, investing in market testing and ad campaigns are great ways to understand and grow your customer base. We recommend having the most reliable sales structure possible set up before you take out a loan since being unable to pay it back on time can seriously disrupt your business growth.

In regards to other types of financing, eCommerce loans may come with high interest rates. This will mostly depend on your company’s current income and your credit score. Any lender will want to take as low a risk on their investment as possible, so knowing that you are already bringing in a significant amount of money reduces the chance that you won’t be able to repay their loan. Some lenders might not even give you capital if your credit score isn’t good enough. Alternatively, others might demand some form of collateral, whether it be your business’ assets or a personal guarantee from you, making you personally liable if your company can’t repay the loan.

How Does a Business Qualify for an ECommerce Loan?

Getting a company to offer you an eCommerce loan depends a lot on their conditions. Almost all of them will factor your credit score into their calculations, and it will directly affect how much money you are eligible for, and how large your interest rate will be. Next, they will take a close look at your business and how well it has been performing in recent times by examining your assets, balance sheet, and sales.

All these factors will help them understand the likelihood of you paying back your loan in full and on time. In order to qualify, you should ensure that you have a good credit score and at least several months of positive sales growth to demonstrate that you are likely to earn back the money needed to repay the loan.

What Kinds of ECommerce Loans Are There?

Fixed-term loans

Fixed-term loans are the most common type of loan you’ll encounter. They involve getting a lump sum from a lender and paying it back in several payments, over an agreed-upon period of time. In essence, all loans follow a version of this model to varying degrees. The hard part is to decide which fixed-term loan is right for your business, and what company to go with. This type of loan is mostly intended for companies that have a plan for what to invest capital into, for example, a new product or larger batches of inventory. It’s a great opportunity to boost the growth you are already seeing and usually comes with reasonable conditions and pricing.

Bank loans

Bank loans are reliable and can reach large sums, but they are hard to get as they require a lot of paperwork. This is because banks require a lot of due diligence, such as checking credit histories, to ensure that you have the financial stability to reliably repay your loans. Unlike other lenders, banks can take several weeks to approve a loan, so if you need a short-term financing option you should look elsewhere.

Banks loans are straightforward, offering a borrower a set amount that is paid back with interest after an agreed-upon time. It will be hard to get approved for a loan if your business is still small. You are more likely to get it if you have assets that can act as collateral in case you don’t manage to repay the whole amount. Bank loans are best for larger eCommerce sellers that see reliable and constant sales.

Invoice factoring

This type of loan is best suited for eCommerce businesses that send invoices to customers and spend up to a few weeks waiting for them to be paid. Any online seller knows that such an amount of time without significant capital coming in can make a huge difference on your ability to reinvest your profits and organize new inventory shipments.

Factoring loans entail that a lender purchases your accounts receivable for a slightly lower amount than they will be worth when paid. This means if several customers have outstanding bills with you for $1000, the lender would buy your accounts receivable for $900, meaning you get hard cash instantly instead of waiting several weeks to get paid. The lender gets the right to the customer payments, making a profit when they end up settling their bills.

SBA loans

SBA (Small business administration) loans are available from banking institutions, credit unions and online lending services. They are only available from within the US and follow strict guidelines, usually involving personal guarantees and collateral assets. Crucially, you need to have good credit or you won’t be eligible for this type of loan. Providers might ask for a down payment as high as 20% of the loan and usually charge additional fees.

While SBA loans can include large sums of money that are repaid over long periods, applying for them takes a lot of time and paperwork. That means they aren’t ideal for small businesses that need short-term cash. If you are more established, have a great credit history, and need large sums, this might be the right option for you.

Equipment financing

This type of loan is only useful if your eCommerce business uses equipment to create its products, for example, sewing machines or 3D printers. A key factor is that said equipment will be used as collateral if you are unable to pay back your loan on time. However, doing so lowers the interest rate you need to pay. Equipment financing offers a lot of leeway in terms of when to repay the full amount, which can be many years down the road.

What is the best option for you?

As you can see, eCommerce loans come in all shapes and sizes. When deciding on which one fits best for your business you need to weigh how much capital you need, how quickly you require it, and what interest rate you can afford. All of these factors affect each other, so you need to balance them against one another.

Is time the biggest concern for you or do you want the lowest interest rate possible? If you have assets to give as collateral, a good credit score and don’t need the money right away, a bank loan might be suitable for you. If you require capital as soon as possible you should look into fixed-term loans or equipment financing, if your business uses physical apparatuses.

Talk to loan providers and try to get an understanding of what offer they can give you. The biggest influence on your deal’s conditions will ultimately depend on the state your business is in already.

A different solution

If you feel that the conditions of an eCommerce loan don’t fit your business, you might want to consider 8fig’s Growth Plan. It entails receiving a capital injection that doesn’t accrue interest; instead you gradually remit a fixed cost of capital over time. 8fig offers a unique formula for eCommerce sellers that provides your business with the financing you need and a payment schedule that can be tailored to your sales. This means you aren’t scheduled to remit until your products start selling.

What truly sets 8fig apart is that it is highly flexible, which means if a hiccup in your supply chain delays your sales there is no need to stress. You can simply adjust your Growth Plan so your next remittance happens in line with your cash flow. All of this happens without a credit score analysis, anything being taken as collateral, or a personal guarantee. 8fig also offers free services that help you get an improved overview of your shipments, supply chain, and business. Check it out today and get the funding you need to take your eCommerce store to the next level.

to our blog

Read the latest

from 8fig

AI is quietly reshaping eCommerce. Karma’s Hadas Bar-Ad explores how today’s sellers are using intelligent tools to streamline operations, boost efficiency, and drive smarter growth.

WhatsApp isn’t just for memes and group chats anymore. With a 98% open rate, it’s the secret weapon your eCommerce marketing strategy might be missing. Here’s how to do it right.

Stuck with extra inventory after Amazon’s Spring Sale? Learn five smart strategies to clear unsold stock, boost cash flow, and avoid future overstocks with smarter inventory planning.